France's AI Bet: Record Investment, Real Risks

Macron announced €93 billion in foreign investment at Choose France. But as AI financing hits $2 trillion globally, economists are asking: is this a bubble?

At a Glance

France’s annual Choose France investment summit, held June 1 at the Palace of Versailles, drew pledges totaling €93 billion (approximately $100 billion) — more than the combined total of all eight previous editions.

Global AI-related investment is expected to surpass $2 trillion this year, with spending on data centers alone up 70% in the past year, heading toward $4 trillion by 2030.

Economists are divided: some see an irrational bubble reminiscent of the dot-com crash of 2000; others argue AI investment reflects genuine long-term technological demand.

This image is used for illustrative purposes only.

Versailles sets a record

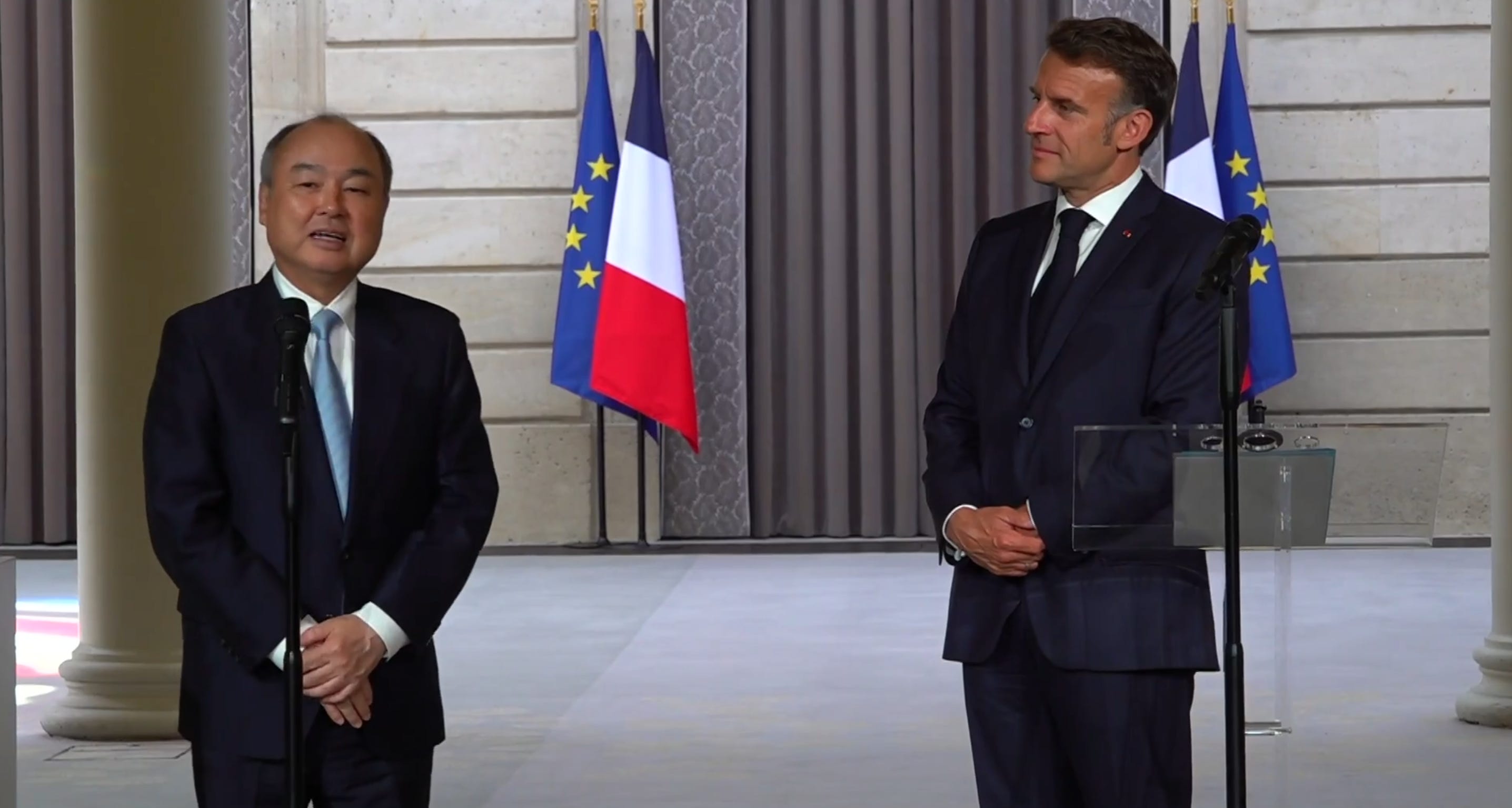

On June 1, 2026, Emmanuel Macron, the president of France, announced at the Palace of Versailles that this year’s Choose France summit had secured €93 billion in confirmed foreign investment commitments, tied to more than 15,000 jobs and 71 new industrial and technology projects. The figure is striking not just for its size but for what it displaces: the eight previous editions of Choose France combined had generated approximately €87 billion in pledges. This edition alone surpassed them all.

Choose France is an annual investment summit created by Macron in 2018 and hosted at Versailles as a deliberate statement of ambition — France’s bid to reposition itself as Europe’s top destination for foreign direct investment, roughly analogous in purpose (if not in format) to the World Economic Forum in Davos.

The headline commitment came from SoftBank, the Japanese technology investment conglomerate led by billionaire Masayoshi Son. The firm pledged €75 billion in France, with €45 billion to be deployed by 2031, concentrated in data centers and artificial intelligence infrastructure.

The shadow of the dot-com crash

That concentration on AI is precisely what some economists find alarming. The question few policymakers raise publicly is this: are the dynamics of 2026 uncomfortably close to those of 2000?

The dot-com bubble followed a pattern now studied in business schools worldwide: massive capital flows toward nascent technology companies, stock valuations decoupled from underlying revenues, the promise of a coming revolution that justified any price. Then the collapse — trillions of dollars in market capitalization wiped out within months, retail investors ruined, and entire sectors of the nascent internet economy reduced to rubble.

Today’s numbers are on a different scale. Global AI-related investment is expected to exceed $2 trillion this year. Data centers — the physical infrastructure that powers AI models — saw investment surge by 70% last year alone. By 2030, total AI investment could reach $4 trillion.

How a bubble works

A financial bubble follows a simple logic: prices rise, which attracts investors, which pushes prices higher — until something breaks the cycle. The disconnect between market price and underlying reality is not a problem until someone names it.

What makes the AI moment harder to read than 2000 is that the leading companies are not fictional. Nvidia posted over $60 billion in revenue last year. The dot-com casualties — Pets.com, Webvan, eToys — had no revenue model at all. The question today is not whether AI companies make money. It is whether their current valuations, which assume decades of compounding dominance, can survive the first serious competitor, the first regulatory shock, or simply the first quarter that disappoints.

A fifteenfold increase in Nvidia’s market capitalization in four years — from $340 billion to more than $5 trillion — is not irrational if you believe the company will supply the infrastructure for every major economy’s AI buildout indefinitely. It is a very large bet on a very specific future.

Two camps, one question

Economists are divided, and intellectual honesty requires presenting both positions.

Skeptics argue that current AI market dynamics carry the hallmarks of irrational exuberance. Stock valuations no longer reflect today’s revenues but projections of massive future adoption that remain hypothetical. Any setback — a disappointing product cycle, unexpected regulation, a high-profile AI failure — could trigger a sharp correction with systemic consequences.

Optimists counter that comparing AI to the dot-com bubble is a category error. Unlike the startup class of 2000, which often had no revenue and no business model, today’s leading AI firms generate substantial income and address real, growing demand across healthcare, logistics, security, and energy. Investment in data centers is physical infrastructure, not pure speculation — it creates jobs, consumes power, and produces tangible assets. The question, on this reading, is not whether to invest, but how to direct investment toward the highest-value applications and under what regulatory and environmental constraints.

What Choose France reveals beyond the numbers

France has spent the better part of a decade trying to shed its reputation as a hostile environment for foreign capital — marked by fiscal instability, rigid labor markets, and a cultural wariness toward finance. The Choose France figures suggest that narrative has shifted. Versailles is working as a signal.

But the record €93 billion figure leaves a harder question unanswered: how much of this investment will translate into durable local employment, skills transfer, and an industrial base rooted in French territory? SoftBank’s data center investment will create jobs, but highly specialized ones, in limited numbers — and data center economics do not automatically redistribute value into the surrounding local economy.

France captures the capital; it does not necessarily capture the value chain.

The Bottom Line

A record €93 billion in a single day is an undeniable political achievement for Macron. But the real question is not about the record — it is about what these capital flows actually build. If AI is genuinely the next industrial revolution, France is well-positioned to be a serious player. If it is a bubble, France will be among the first to feel the consequences when it bursts. The difference between those two scenarios will not be visible at Versailles. It will be visible when the first major data center project is mothballed, when a sovereign wealth fund quietly marks down its AI portfolio, or when a European government has to decide whether to bail out infrastructure it invited in with fanfare and cannot afford to let fail.

Sources: France Info · France Télévisions